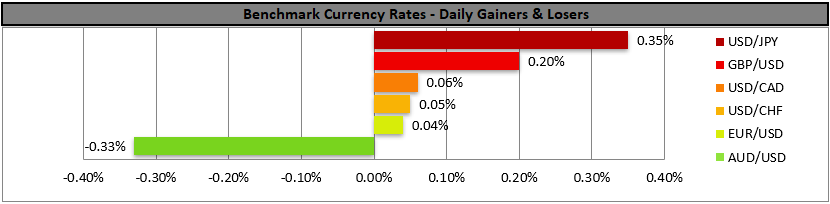

February’s US employment report in focus as global markets remain sensitive to geopolitical tensions and economic signals. Investors are closely watching the upcoming NFP release for clues about the strength of the US labor market and the potential direction of the USD. The data could play a key role in shaping market sentiment during the early American trading session.

February’s US employment report could move the USD

Amidst the chaos in the markets created by the US-Iranian conflict, the USD was on the rise yesterday, supported by fresh safe-haven inflows.

Today, we highlight the release of the US employment report for February with its NFP figure, and should the readings show a tighter-than-expected US employment market, we may see the USD getting renewed support in the early American session.

Risk off sentiment causes US stock markets edge lower

Oil prices continued to climb yesterday as the Iranians hit another oil tanker, practically threatening oil shipping in the Straits of Hormuz and the Persian Gulf in general.

Oil market worries tended to intensify pushing oil prices higher as the scenario for further downsizing of oil production by Gulf countries intensifies. Should we see the oil market’s worries intensifying even further we may see oil prices getting more support.

Bitcoin’s price corrects lower

Bitcoin’s price corrected lower yesterday and during today’s Asian session, leaving crypto traders wondering as it has set its latest rally under pressure.

We see the crypto’s price being in a make-or-break position as on the one hand the bullish tendencies have not been totally erased yet, yet the crypto has failed to make a decisive upward movement.

Other highlights for today

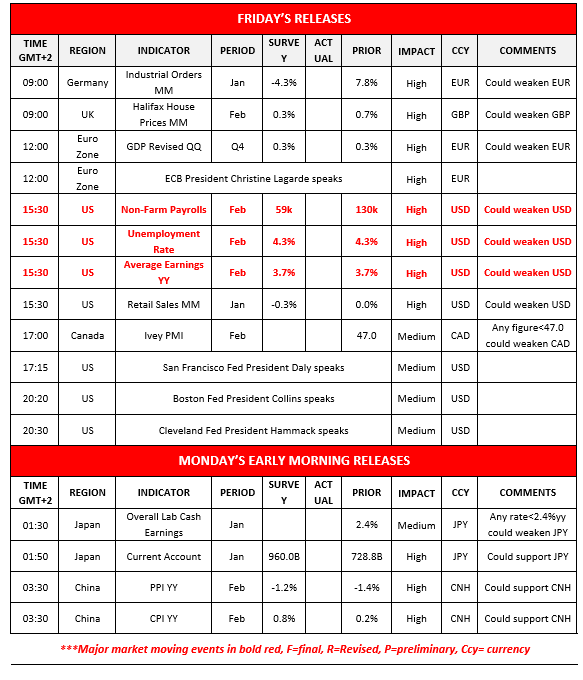

Today we get Germany’s industrial output for January, UK’s Halifax House Prices for February, Euro Zoe’s revised GDP rate for Q425, the US retail sales for January and Canada’s Ivey PMI figure for February.

On a monetary level, we note that ECB President Christine Lagarde, San Francisco Fed President Daly, ECB Board Member Schnabel, Boston Fed President Collins and Cleveland Fed President Hammack are scheduled to speak.

In tomorrow’s Asian session, we get Japan’s current account balance and overall labour cash earnings, both being for January as well as Chinas’ inflation metrics for February.

Charts to keep an eye out

Dow Jones dropped yesterday breaking the 48350 (R1) support line, now turned to resistance.

We maintain a bearish outlook for the index given that the downward trendline guiding it remains intact and the RSI indicator is nearing the reading of 30, implying strengthening bearish market sentiment for the Index.

On the other hand the price action has reached the lower Bollinger band which may slow down the bears. We set as the next possible target for the bears the 47150 (S1) support line while for a bullish outlook, which we currently see as remote, the index has to breach the 48350 (R1) resistance line and continue higher to reach if not breach the 49600 (R2) resistance level.

WTI’s price surged yesterday and during today’s Asian session, at some point testing the 80.00 (R1) resistance line. We maintain our bullish outlook for the commodity’s price action, yet also view it as being at overbought levels and thus ripe for a correction lower.

Should the bulls maintain control over WTI’s price we may see it breaking the 80.00 (R1) line and start aiming for the 83.85 (R2) level.

Should the bears take over, we may see it breaking the steep upward trendline guiding it in a first signal that the upward motion was interrupted and continue to break also the 76.60 (S1) line and start aiming for the 73.35 (S2) support level.

Dow Jones Daily Chart

- Support: 47150 (S1), 45750 (S2), 44580 (S3)

- Resistance: 50535 (R1), 49600 (R2), 48350 (R3)

WTI Daily Chart

- Support: 76.60 (S1), 73.35 (S2), 70.00 (S3)

- Resistance: 80.00 (R1), 83.85 (R2), 87.10 (R3)

Isenção de responsabilidade:

Esta informação não é considerada como aconselhamento ou recomendação ao investimento, mas apenas como comunicação de marketing. O IronFX não é responsável por quaisquer dados ou pela informação fornecida por terceiros aqui mencionados, ou com links diretos, nesta comunicação.