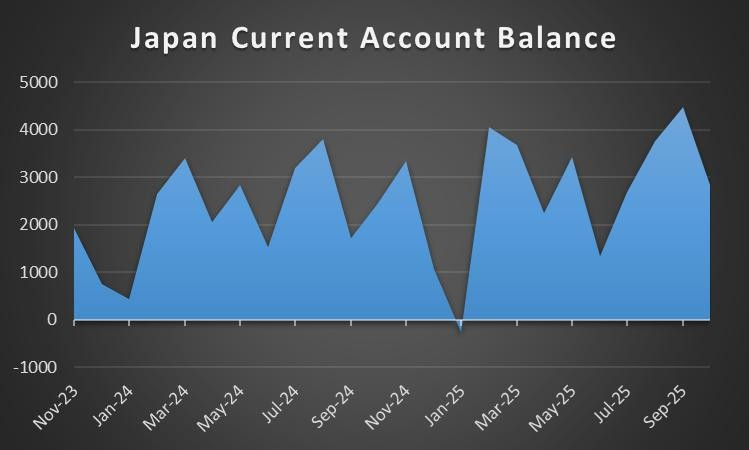

The week is drawing to a close and we open next week’s calendar. On Monday we get Euro Zone’s Sentix index for January and on Tuesday we note the release of Japan’s current account balance for November, the Czech Republic’s final CPI rates for December and we highlight the release of the US CPI rates for the same month. On Wednesday we note the release of China’s December trade data for December and from the US the PPI rates for November and retail sales for the same month. On Thursday, we get Japan’s PPI rates for December, UK’s GDP and manufacturing output growth rate for November, Canada’s House starts for December, from the US the weekly initial jobless claims figure and the Philly Fed Business index for January and Canada’s manufacturing sales for November. On Friday we get the US industrial output for December and Germany’s Full Year GDP rate for 2025.

USD – CPI rates for December to set the stage

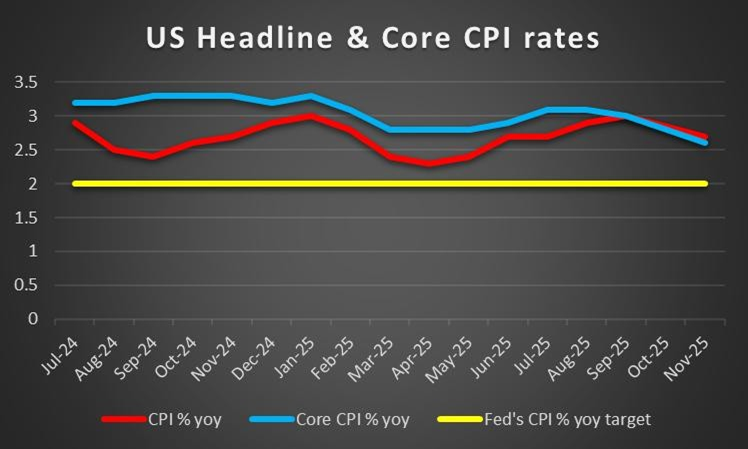

On a fundamental level, we are obviously going to note the developments over this past weekend, where the US military deposed and extracted Venezuelan President Maduro, who is now facing drug-related charges in a court in New York. The decision by the US has effectively reminded the world as to who is in charge. In turn, should Venezuela open up to investments by US companies, certain stock prices may find some support. On a macroeconomic level, we would like to note the release of the US CPI rates for December which are due out next Tuesday. The CPI rates are key to deciphering the inflation narrative within the US economy and could have severe implications for the markets depending on the picture which emerges. In particular, should the inflation release showcase an acceleration of inflationary pressures within the US economy, it may provide support for the dollar as pressure may mount on the Fed to maintain their monetary policy stance unchanged. On the other hand, should the inflation print showcasing easing inflationary pressures within the US economy, the opposite scenario may take hold and could thus weigh on the dollar. We should also note that the US Employment data for December is set to be released later on today and could heavily influence the dollar’s direction as the week comes to a close. Specifically, the NFP figure is expected to come in lower than the prior figure, whilst the unemployment rate is expected to decrease, essentially resulting in a mixed employment market picture. Hence, a mixed picture could lead to heightened trading volatility. However, our focus would be mainly on the unemployment rate, as the anticipated reduction could take over the narrative and could thus provide some support for the dollar, or mitigate the bearish implications of the NFP figure.

Analyst’s opinion (USD)

“The anticipated mixed employment market could bolster the Fed’s intentions to remain on hold, yet the inflation print on Tuesday could sway the pendulum in either direction. Moreover, given that Fed Chair Powell’s term is set to end this year, should a Fed Chair be announced in the coming week the markets may be more preoccupied with his/her statements rather than the financial releases. Geopolitically, the US reminded US why they are No.1, but their meddling in South America could push gold prices should instability arise or further action against ‘unfriendly’ nations are taken”

GBP – GDP rates due out next week

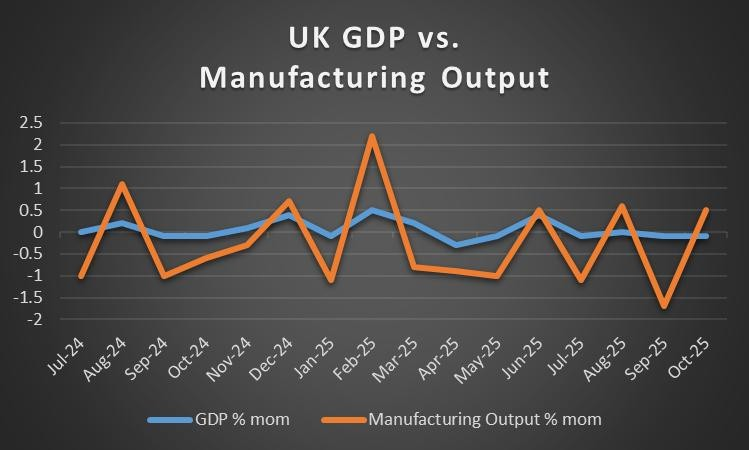

The UK’s GDP rates for November are due to be released next Thursday and may be of interest for Cable traders. The GDP rate, although on a month-on-month basis can still provide insight into the state of the UK economy and thus should the rate showcase an improvement from the prior reading of -0.1% and imply economic growth, it may be seen as a positive for the UK economy which in turn could provide support for the sterling. However, on the other hand should the GDP rate remain in contraction territory, it could spell trouble for the UK economy and could thus weigh on the sterling. On a fundamental level, reports have emerged per POLITICO that the UK is preparing a bill establishing a legal framework for UK-EU alignment, in an attempt to reset its relationship with the EU, which could lead to some political issues down the line, yet no immediate market impact.

Analyst’s opinion (GBP)

“The UK’s GDP rates are interesting but not necessarily a market mover. Nonetheless, considering the situation in which the UK Labour Government has put itself in, they need a ‘win’ here and thus an improvement could provide support for the sterling, whereas a lower than anticipated figure or even a continued contraction in the economy could weigh on the pound.”

JPY – BOJ eyes more rate hikes

On a monetary policy level, we would like to note that the BOJ is its quarterly regional report which was released yesterday stated that “All nine regions reported that their respective economies have been recovering moderately, picking up, or picking up moderately, although some weakness had been seen in part”. The comments within the BOJ’s report showcase that in terms of economic activity there has been some recovery, which in turn could pave the way forward for the bank to maintain their rate hiking approach. Therefore, should BOJ policymakers showcase a clear willingness to hike rates in their next meeting it may provide support for the JPY. On a fundamental level, Japan’s relationship with China has continued to deteriorate as China has banned “exports of dual-use items to Japan that can be used for military purposes”, with Japan calling the ban “absolutely unacceptable”. The continued deterioration of the relationship with China could lead to negative impacts on the Japanese economy and may have thus contributed to the weakening of the JPY. Moreover, with sources reporting that China is considering a further clampdown on exports of rare earths to Japan the JPY may be further weakened as the Japanese economy is reliant on rare earth imports from China. Hence the relationship between Japan and China warrants further monitoring as an escalation could weigh on the JPY.

Analyst’s opinion (JPY)

“We see the case for sticking on their rate hike path considering the BOJ’s report which emerged earlier on this week. However a trade war with China and a deterioration of Japan’s relationship with a key trading partner could lead to unwanted effects on the economy. Hence, possible ‘hits’ to the Japanese economy could outweigh hawkish commentary as the BOJ’s decisions could be influenced should the economy appear to be heading to a ‘bad’ place. In our view, the JPY may weaken for some time but overall with the BOJ possibly hiking rates this year, we wouldn’t be surprised to see the JPY strengthening down the line.”

EUR – Eurozone Sentix index to be released Monday

On a fundamental note, the rotating EU Council Presidency has moved to the Republic of Cyprus which now embarks on its 6-month term. The Republic of Cyprus takes over as the EU’s next seven-year budget looms and which will be decided by the end of the term in June 2026 where an EU leader summit is set to take place. Hence, some attention is warranted to any developments emerging from the island, as the EU’s budget policy may influence the common currency. On a macroeconomic level, we would like to point out that France’s, Germany’s and the Eurozone’s preliminary CPI rates for December failed to meet expectations set by economists implying that inflation may be easing in the in the Zone in general and it’s two largest economies. The lower- than-anticipated inflation print may have weighed on the common currency, as the option for the ECB to cut if they wished to continues to be open. In turn should, sentiment from ECB policymakers appear to be dovish in nature, it could further weigh on the common currency. For next week, trader’s may be interest in the release of the Zone sentix figure.

Analyst’s opinion (EUR)

“Even with the CPI rates coming in lower than expected, we are not convinced that the ECB will proceed with a rate cut in their next meeting. In our view the bank is ideally positioned at their current interest rate levels to deal with and combat inflation and a rate cut at this point may be premature, hence we wouldn’t be surprised to see the overall rhetoric from the ECB noting that they are in a ‘good place’.”

AUD – Fundamental’s to lead the Aussie in the coming week

On a fundamental level, we should note that Australia is currently battling with an intense heatwave as temperatures have soared to above 40 degrees Celsius, leading to warnings of “extreme fire danger”, with the FT reporting that towns have already been evacuated and the fire risk being expected to peak today. On a macroeconomic level, we would like to note the release of Australia’s CPI rates for November with the monthly indicator coming in lower than expected, which tended to imply easing inflationary pressures in the Australian economy. In turn, implications of easing inflationary pressures in the Australian economy may have aided in the Aussie’s weakening against the dollar during the week. Moreover, sticking to our macroeconomic theme the nation’s trade balance for November came in lower than expected but still noted a trade surplus. Nonetheless, the reduction in exports from 2.8% to -2.9% may have weighed on the Aussie considering the nation’s status as an exporter of raw materials. In turn should the exports rate continue to worsen, it may be reflected in the Australian dollars price.

Analyst’s opinion (AUD)

“The exports rate is a concern for Aussie traders and the negative rate posted this week may spark some concern unless an improvement is noted in the next release.”

CAD –Manufacturing sales rate due out on Friday

On a macroeconomic level, Canada’s Ivey PMI figure for December was released this Wednesday and came in better than expected.The figure did not only exceed expectations by economists but also escaped contraction territory and now showcases an expansion of the Canadian manufacturing sector, which could be seen as a positive for the economy. Hence the better than expected figure could provide some support for the Loonie or have mitigated some of the dollar’s strengthening during the week. Moreover, we should note that the time of this report the Canadian employment data for December has not yet been released and could thus change our overall stance on the state of the Canadian economy. For next week traders may be interested in the release of the Manufacturing sales rate next Friday, although considering it’s low impact nature, CAD traders may be more interested in releases stemming from other nations.

Analyst’s opinion (CAD)

“The Canadian economy appears to be faring all right for the time being, considering the Ivey PMI figure for December. Should they keep it up and showcase further improvements in the manufacturing sector the Loonie could gain. Although in our view, considering their neighbour, any external pressures could also influence the CAD, especially the oil narrative, considering Canada’s status as an oil exporter.”

General Comment

The markets have been rocky, especially the oil market following the US’s intervention in Venezuela. The situation remains volatile as the nation’s future is being decided behind closed doors in Washington, thus influencing gold and oil prices respectively. Moreover, the protests in Iran appear to be escalating and thus should we see a regime change occurring over the weekend, it could lead to very high volatility in the markets once the markets re-open and thus the situation warrants close attention.

If you have any general queries or comments relating to this article please send an email directly to our Research team at research_team@ironfx.com

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.