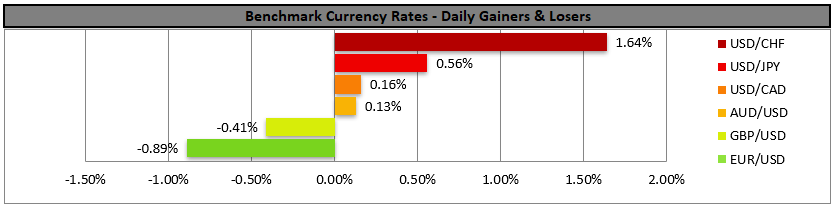

USD continues to strengthen in the FX market

The USD continued to strengthen in the FX market in today’s Asian session albeit with less intensity as increased worries for US inflationary pressures and the Fed’s intentions tend to lift the greenback.

Today we note the release of the Euro Zone’s preliminary HICP rates for February and the rate is expected to remain unchanged below the ECB’s target which could weigh on the common currency somewhat.

Across the Channel, UK Chancellor of the Ex Chequer Reeves is to deliver her Spring Statement in an effort to generate trust in the UK economic outlook and if actually so could provide some support for GBP.

Equity market’s confidence remains shaken

US equities recovered some ground yesterday, yet edged lower once again in today’s Asian session. Overall market confidence remains shaken and a cautious approach seems to dominate market participants as a prolonged US-Iranian conflict may rekindle inflationary pressures thus press the Fed to keep rates high for longer, while increased oil prices may imply lower profitability. Should we see market worries intensifying further we may see US equities losing further ground.

Oil bulls maintain momentum

Oil prices were on the rise in today’s Asian session as market worries for the supply side of the international oil market remain present. The possibility of a prolonged conflict may result to increased shipping costs, a possible closure of the Straits of Hormuz and less activity from oil refineries in the region, all threatening the supply chains of the international oil market. Should we see the threats to global oil supply intensifying, for example if the Iranians try to mine the Straits of Hormuz, we may see oil prices getting further support.

Bitcoin remains stable

Bitcoin’s price edged higher yesterday, reportedly enjoying ETF inflows amidst geopolitical risk and uncertainty in the US economic outlook. The wide discussion among crypto traders is whether the ETF inflows are signaling trust that the crypto king’s price action has allready bottomed out and the bearish cycle is more manageable rather than systemic, which in turn could lead to more gains for the crypto-market.

Other highlights for today

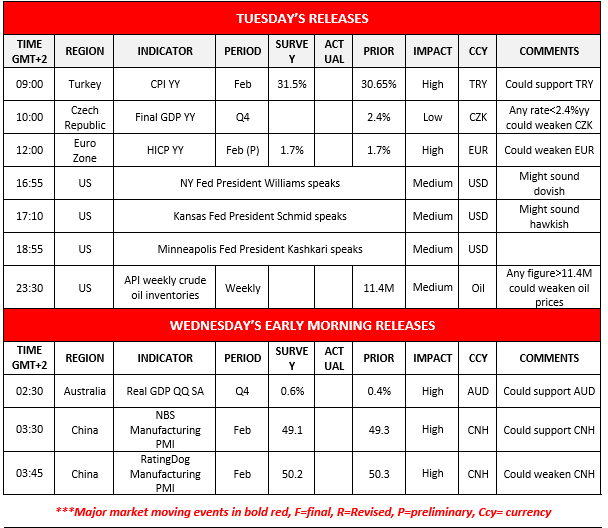

Today we get Turkey’s CPI rates for February, the Czech Republic’s GDP rates for Q4 and the weekly API crude oil inventories. On a monetary level, we note that NY Fed President Williams, Kansas Fed President Schmid and Minneapolis Fed President Kashkari are scheduled to speak. On Wednesday’s Asian session, we get Australia’s GDP rates for Q4 and China’s NBS and Rating Dog manufacturing PMI figures for February.

Charts to keep an eye out

WTI’s price rose corrected lower after its initial rally yesterday, yet in today’s Asian session the bulls pushed the commodity’s price towards the 73.35 (R1) resistance line.

The RSI indicator remained above the reading of 70, implying a strong bullish market sentiment yet also that WTI’s price is at overbought levels.

Should the bulls maintain control, we may see WTI’s price breaking the 73.35 (R1) resistance line and start aiming for the 76.60 (R2) resistance base.

Should the bears be in charge, we may see WTI’s price breaking the 70.00 (S1) support line and continue to break also the 66.20 (S2) level.

GBP/USD dropped yesterday breaking the 1.3385 (R1) support line, now turned to resistance. WE intend to maintain a bearish outlook for cable as long as the downward trendline guiding it remains intact.

Should the bears remain in charge we may see GBP/USD aiming if not breaking the 1.3190 (S1) support line.

Should the bulls take over we may see GBP/USD reversing course, breaking the 1.3385 (R1) resistance line, breaking also the prementioned downward trendline and reach if not breach the 1.3590 (R2) level.

WTI Daily Chart

- Support: 70.00 (S1), 66.20 (S2), 61.80 (S3)

- Resistance: 73.35 (R1), 76.60 (R2), 80.00 (R3)

GBP/USD Daily Chart

- Support: 1.3190 (S1), 1.3010 (S2), 1.2870 (S3)

- Resistance: 1.3385 (R1), 1.3590 (R2), 1.3790 (R3)

Disclaimer:

This information is not considered as investment advice or an investment recommendation, but instead a marketing communication. IronFX is not responsible for any data or information provided by third parties referenced, or hyperlinked, in this communication.