Next week’s calendar is packed with releases of high impact financial data and interest rate decisions from various central banks. On Monday we get Japan’s Tankan indexes for Q4, China’s industrial output for November, Euro Zone’s industrial output for October and Canada’s CPI rates for November. On Tuesday we get Japan’s, France’s , Germany’s, the Euro Zone’s, the UK’s and the US preliminary PMI figures for December as well as UK’s employment data for October, Germany’s ZEW indicators for December and from the US we highlight the release of the US employment report for November, with its NFP figure and also note the release of the retail sales for October. On Wednesday, we get Japan’s trade data for November, UK’s CPI rates for November, Germany’s Ifo indicators for December and New Zealand’s GDP rate for Q3. On Thursday we get the interest rate decisions of Sweden’s Riksbank, Norway’s Norgesbank, UK’s Bank of England, the Euro Zone’s ECB and the Czech Republic’s CNB. Also on Thursday we note from the USD, the release of the CPI rates for November, the weekly initial jobless claims figure and the Philly Fed Business index for December. On Friday we get Japan’s CPI rates for November, BoJ’s interest rate decision, Germany’s Gfk consumer confidence for January, UK’s November retail sales, the US CPI rates for October, Canada’s retail sales for October and the Euro Zone’s preliminary consumer confidence for December.

USD – CPI and employment data to shake the USD

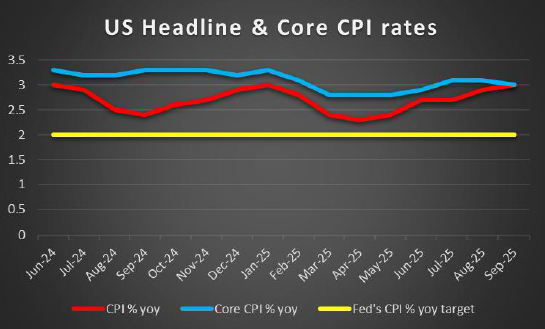

The USD seems to be in the reds against its counterparts for the third week in a row, as the Fed’s interest rate decision on Wednesday seems to be setting the greenback under pressure. The bank as was widely expected, cut rates by 25 basis points, yet its forward guidance seems to raising doubts about the pace of further easing of its monetary policy in the next year. It’s characteristic that the new dot plot shows that Fed policymakers are expecting rates to drop by only 25 basis points in the coming year, while the market before the decision was expecting another three rate cuts. Should we see in the coming days Fed policymakers stressing the possibility of a slower rate cut path or even no rate cuts, we may see the USD getting some support. Yet we have to note that we expect substantial turbulence in the coming year for the Fed, given the replacement of Fed Chairman Powell but also the Fed’s rotation system. In the coming week we get a number of high impact US financial data which could shake the markets as they focus on the main areas of interest of the Fed, namely inflation and employment. We make a start with US employment report for November, as economists expect the US employment market to loosen further with the NFP figure dropping to 35k if compared to September’s 119k and the unemployment rate to remain unchanged at 4.4%. Should the actual data show a wider slack than expected in the US employment market we may see the release weighing on the USD as it could enhance the market’s expectations for the Fed to cut rates at a faster pace. On the other hand we also note the release of the US CPI rates for November on Thursday and should the rates fail to slow down, implying a resilience of inflationary pressures in the US economy we may see the USD getting some support.

Analyst’s opinion (USD)

Overall we see the case for the USD to remain under pressure in the coming week, yet once again we highlight the financial data due out as key issues that could alter the greenback’s direction to either side.

GBP – BoE expected to cut rates

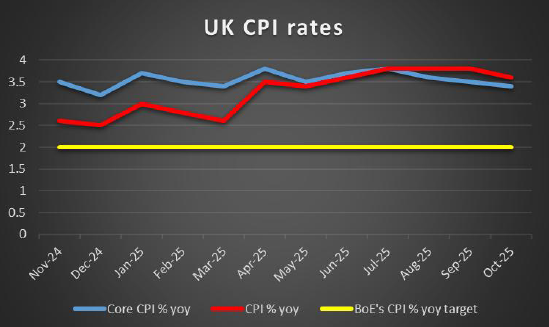

The pound sent some mixed signals in the past week as it strengthening against the USD, and JPY, yet is in the reds against the EUR. In the coming week, we highlight the release of BoE’s interest rate decision, next Thursday as a key event for pound traders. The bank is expected to cut rates by 25 basis points and currently GBP OIS imply a probability of 92.2% for such a scenario to materialise. Yet GBP OIS also imply that the market expects the bank to proceed with another rate cut in 2026, one only, which tends to imply that the market’s expectations for the bank’s intentions continue to lean on the dovish side. We note that the bank is at cross roads as on the one hand, inflation remains high providing hawkish innuendos for the bank, yet on the other hand, growth remains anemic adding pressure on the bank to ease its monetary policy further. Hence should the bank cut rates as expected we intend to turn our focus to the bank’s forward guidance. Should the bank imply in its forward guidance imply that more easing lays ahead for its monetary policy we may see the pound retreating, while a more hawkish tone could provide some support for the sterling. Also we intend to keep a close eye on the votes in favour of a rate cut and the ones favouring the bank remaining on hold as it would allow a deeper insight in the balance of power between doves and hawks. On a macroeconomic level, we note two releases which we consider key. The first would be the release of October’s employment data on Tuesday, and a possibly tighter than expected UK employment market could provide some support for the pound. Also on Wednesday, we get UK’s November CPI rates and a possible acceleration could provide some support for the pound ahead of BoE’s interest rate decision next Thursday.

Analyst’s opinion (GBP)

The pound over the past few days seemed to be gaining some support against its counterparts, yet its direction in the next week may prove difficult to predict. BoE’s interest rate decision, the release of inflation and employment data all tends to cloud the path of the pound. A possible rate cut and a subsequent dovish forward guidance from the BoE could weigh on the sterling, as could a possible easing of inflationary pressures and a looser employment market.

JPY – BoJ: To hike or not to hike?

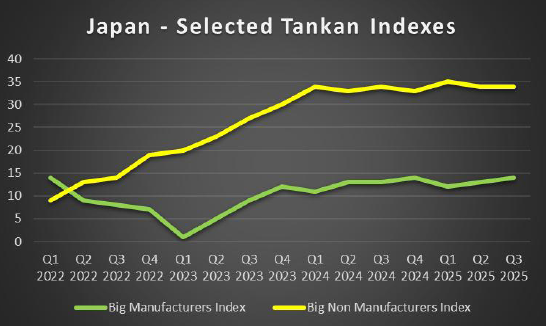

JPY sent some mixed signals this week as it remained relatively stable against the USD, yet lost ground against the GBP and EUR. In the coming week, BoJ’s interest rate decision may prove the main event for JPY traders. The bank is expected to hike rates by 25 basis points and currently JPY OIS imply a probability of 79.8% for such a scenario to materialise and also imply that the market expects the bank to continue hiking once maybe twice in the coming year. We are a bit more conservative and expect one more rate hike in the coming year, yet the overall idea here is that the market’s expectations are leaning on the hawkish side after next Friday’s interest rate decision. At this point we have to note that the bank’s hawkish intentions had faced headwinds from the Japanese Government. Yet the weakening of JPY against the USD since the midst of September and the relative inflationary pressures may allow the Japanese government to tolerate a possible rate hike, yet the negative growth for Q3, tends to add more pressure on the bank to keep rates low. It should be noted that BoJ Governor Ueda seems to be a firm supporter of higher rates, and has stated recently that the Japanese economy has weathered the shock of US tariffs, a statement that could allow the bank to proceed with a rate hike next Friday. Hence our base scenario is that the bank is to hike rates on Friday and we also expect the bank to issue a forward guidance possibly leaning on the hawkish side and both elements could provide support for the JPY. On a macro level, we note the release of Japan’s Tankan indexes for Q4 and November’s CPI rates next Friday with the latter probably being overshadowed by BoJ.

Analyst’s opinion (JPY)

We highlight the release of BoJ’s interest rate decision as the highlight for JPY traders next week and a rate hike in combination with a possibly hawkish forward guidance could provide some support for the Yen.

EUR – ECB expected to keep its monetary policy in “a good place”

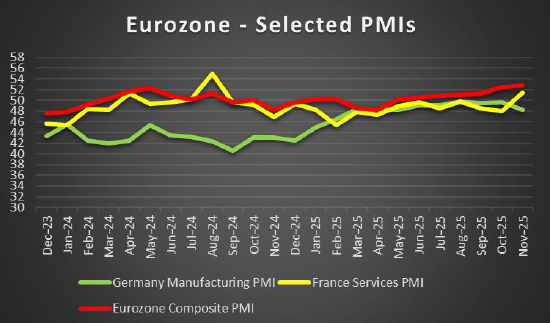

The common currency has strengthened against the USD, the JPY and the pound in a sign of wider strength. In the coming week the main event for EUR traders is expected to be the ECB’s interest rate decision next Thursday, yet before that we note the release of Euro Zone’s preliminary PMI figures for December next Tuesday. The indicators are expected to provide a picture for the level of economic activity and we intend to focus on the indicators for Germany’s manufacturing sector, France’s services sector and for a rounder view the composite index of the Euro Zone as a whole. Main point of worries is the contraction of economic activity for Germany’s manufacturing sector. Overall should we see economic activity in the Zone deteriorating we may see the common currency weakening. Back to ECB’s interest rate decision the bank is widely expected to remain on hold and the market expects the bank to keep rates on ice until the end of next year. Should we see the bank also in tis forward guidance, with “forward guidance” including ECB President Lagarde’s press conference, verifying such market expectations, we may see the EUR getting some support. Also on a more fundamental level, we note the negotiations for a possible peace plan in Ukraine and a possible break through or reports of progress could provide some support for the single currency.

Analyst’s opinion (EUR)

On a macro level we note the release of the preliminary PMI figures for December of Germany, France and Euro Zone as a whole. A possible easing of economic activity could weigh on the EUR. On a monetary level, we highlight the release of the ECB’s interest rate decision and should the bank enhance the market’s expectations for the bank remaining on hold for a longer period we may see the EUR getting some support.

AUD – Fundamentals to lead the Aussie

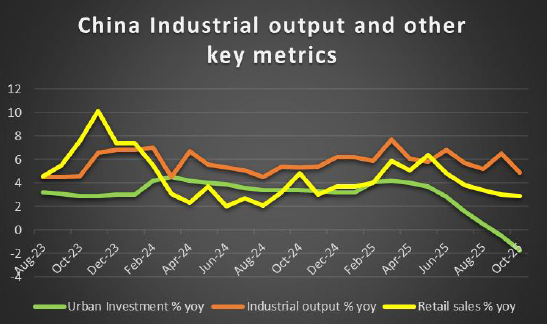

The Aussie continues to be in the greens for a third week in a row against the USD. In the coming week on a macroeconomic level, we note that November’s employment data sent some mixed signals, as the employment change figure dropped into the negatives while the unemployment rate ticked down and the release tended to weigh on the Aussie at the time. In the coming week we note the release of the December preliminary PMI figures and an expediting of the expansion of economic activity could provide some support for the Aussie. On a monetary level RBA decided to remain on hold and RBA Governor Bullock clearly showcased that the rate hike option is on the table, turning the decision into a hawkish standing pat. In the coming week, we note that we have a couple of RBA policymakers scheduled to make statements on Monday and Tuesday and a possible hawkish tone could provide some support for AUD. On a more fundamental level, we note that the Aussie could benefit from a more optimistic, risk on approach by the markets given that it’s considered a riskier asset in the FX market as it’s considered a commodity currency. Also given the close Chinese-Australian ties, we may see Aussie traders keeping a close eye on developments in China. Please note that on Monday we get a number of interesting financial data from China, including the house prices, industrial output, retail sales and urban investment growth rates all being for November. A possible acceleration of the rates could also provide some support for AUD.

Analyst’s opinion (AUD)

RBA’s hawkish on hold tended to be supportive for AUD, and hawkish comments by RBA policymakers in the coming week could provide some support for the Aussie. In the coming week we may see fundamentals leading the Aussie given the light calendar in regards of financial releases and a possible risk on market sentiment could provide some support for the Aussie.

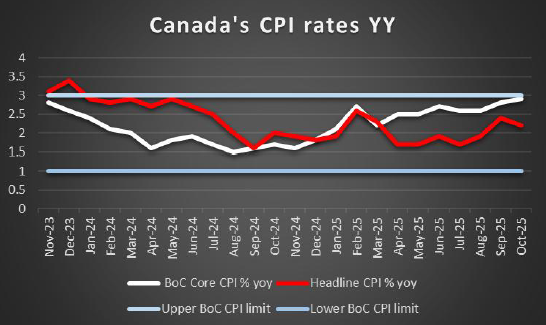

CAD –Canada’s November CPI rates to move the Loonie

Also the Loonie continued to strengthen against the USD for a third week in a row. The Canadian Dollar lost some ground at the time of the release of BoC’s interest rate decision yet started to strengthen afterwards. Overall, the market’s expectations for the bank to remain on hold until September and then hike rates remained unchanged, is a scenario that tends to be supportive for the Loonie, especially should one compare the monetary policy outlook of BoC with the Fed. In the coming week we highlight the speech of BoC Governor Tiff Macklem next Tuesday at the Chamber of Commerce of Metropolitan Montreal and any hawkish comments could provide some support for the Loonie. On a macroeconomic level, we note that the release of the CPI rates for November on Monday and a possible acceleration of the rates could provide some support for the CAD. Also we note the release of December’s business barometer, and retail sales growth rate for October on Thursday and Friday respectively which could provide some volatility for the CAD. On a more fundamental level, we note the drop of oil prices for the week and given the status of Canada as a major oil producing economy, a continuation of the bearish tendencies for oil prices could weigh on the CAD.

Analyst’s opinion (CAD)

In the coming week we highlight the release of Canada’s October CPI rates on Monday and a possible acceleration of the rates could provide some support for the CAD. On a monetary level, we may see also BoC Governor Macklem’s speech next Tuesday and any hawkish comments could also provide some support for the CAD

General Comment

Overall and as an epilogue, we expect the USD to maintain its dominance in the FX market. The frequency and gravity of high impact US financial releases in conjunction with planned comments of Fed policymakers, may keep interest in the FX Market revolving around developments in the US and the greenback. Nevertheless, there also high impact release from other economies that may allow other currencies to come under the spotlight, thus creating a more balanced trading mix in the FX market. As for US equities, we tend to get mixed signals, with Netflix, Warner Bros and Paramount, as well as Oracle being the highlights in the past few days. At this point we note that our main worries are for the slump of Oracle’s share price, as it was a painful reminder of the scenario of a possible bubble existing in the US equity markets, especially among tech companies, as investments in AI may take longer than expected to boost profitability. The market worries are intensified as the tech sector is highly leveraged, increasing the risk factor. A more positive market sentiment may provide some support for US stock markets in the coming week, while should worries intensifying we may see US equities retreating. At the same time the weakening of the USD seems to have finally kicked in, providing some support for gold’s price. We still consider the market’s dovish expectations for the Fed’s intentions as a key factor underpinning the rise of the price of the precious metal, while geopolitics, especially in Ukraine and Venezuela could drive safe haven flows for gold’s price.

이 기사와 관련된 일반적인 질문이나 의견이 있으시면 저희 연구팀으로 직접 이메일을 보내주십시오 research_team@ironfx.com

면책 조항:

본 자료는 투자 권유가 아니며 정보 전달의 목적이므로 참조만 하시기 바랍니다. IronFX는 본 자료 내에서 제 3자가 이용하거나 링크를 연결한 데이터 또는 정보에 대해 책임이 없습니다.